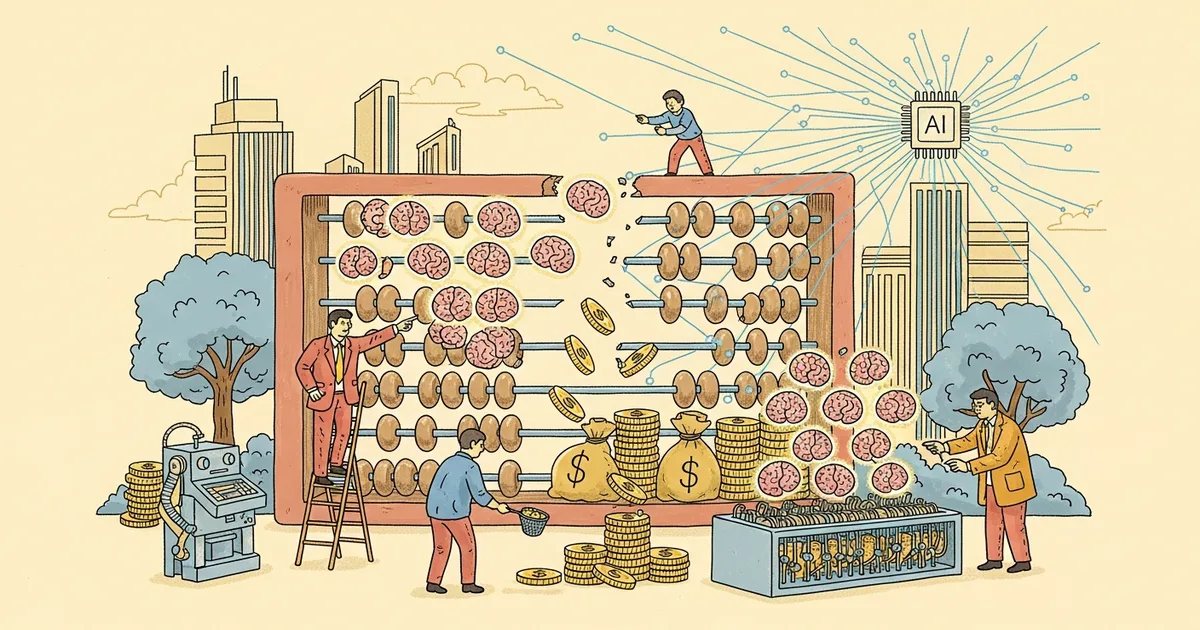

- Economist Daniel Homola argues that AI is collapsing the historical link between cognitive ability and wealth, predicting the IQ-to-income coefficient will fall from 0.35 to 0.10-0.20 within a decade while the wealth coefficient rises from 0.45 to approximately 0.65.

- The essay uses probability theory to show that biological traits follow bell curves while wealth follows power laws, meaning inherited wealth compounds without regression to the mean.

- Homola identifies a 5-to-10-year window where domain experts with AI fluency can still leverage the credential-to-wealth pathway before it closes permanently.

- U.S. programmer employment fell 27.5 percent between 2023 and 2025, cited as early evidence of the thesis in action.

What Happened

Economist Daniel Homola published a 54-minute analysis on March 21, 2026, arguing that artificial intelligence is dismantling the two-century-old connection between cognitive ability and wealth accumulation. The essay, titled “Your Bridge to Wealth Is Being Pulled Up,” uses probability theory and mathematical modeling to predict that the credential-based pathway from intelligence to wealth will close within the next decade, leaving inherited wealth as the dominant determinant of economic outcomes.

“The IQ premium in the labour market is collapsing. The capital premium is not,” Homola writes. “The coefficient on inherited wealth in the income equation is rising as the coefficient on cognitive ability falls — and the transition is measured in years, not decades.”

Why It Matters

Homola’s central thesis rests on the mathematical distinction between two inheritance systems. Biological traits like intelligence follow Gaussian distributions and regress toward the mean each generation. Wealth follows power laws and compounds without regression, transmitted through property law rather than genetics. “Most of the traits you were born with — intelligence, conscientiousness, height — follow a bell curve,” he writes. “Wealth follows a power law.” The top 1 percent of American households holds more than the bottom 50 percent combined, with the mean being five times the median.

The essay traces how credential systems from the 19th and 20th centuries created an unprecedented bridge: “For the first time at scale, cognitive ability could escape the class it was born into.” This pathway operated through the sequence IQ to credentials to income to heritable wealth. Homola argues that large language models now “match median professional performance on the routine tasks that constitute a large fraction of professional billing across legal research, financial analysis, software engineering, and diagnostic reasoning.”

Technical Details

Homola presents an income model expressed as: log(income) = 0.35 times IQ + 0.25 times conscientiousness + 0.45 times wealth + error. He predicts that AI will drive the IQ coefficient from 0.35 down to 0.10-0.20 by the mid-2030s, while the wealth coefficient rises from 0.45 to approximately 0.65. He identifies a critical threshold of roughly $20,000 in net worth that separates subsistence, where savings cannot occur, from the compounding tier where Piketty’s r-greater-than-g mechanism activates.

As supporting evidence, Homola cites U.S. programmer employment falling 27.5 percent between 2023 and 2025, robotics startups raising over $6 billion in the first seven months of 2025, and Federal Reserve data showing median U.S. household wealth of $193,000 versus a mean of $1.06 million. He draws on work from economists Raj Chetty on intergenerational wealth elasticity, Thomas Piketty on capital returns exceeding growth, and Fagereng, Mogstad, and Ronning on pre-marriage wealth correlation operating independently of education.

Who’s Affected

Homola identifies professionals whose work consists primarily of routine cognitive tasks as most immediately exposed: junior lawyers performing legal research, financial analysts, software engineers, and diagnosticians. He rates their AI exposure at 8 to 9 out of 10. The essay argues this creates a narrow arbitrage window for individuals who combine “deep domain knowledge with AI fluency,” a combination he describes as “currently scarce in a way that inherited wealth cannot buy.”

The analysis also challenges policy assumptions. Homola argues that universal basic income and capital taxation can compress wealth distribution from both ends but cannot create new entrants into wealth-generating tiers once the labor-income pathway closes. The window for restructuring inheritance law closes simultaneously with the economic window for individual action.

What’s Next

Homola estimates the arbitrage window at “the next five to ten years,” after which “the legal inheritance system runs alone.” He frames his predictions as falsifiable: if the IQ-to-income coefficient does not decline measurably by 2030, or if the wealth coefficient does not rise, the thesis fails. Whether this framework proves correct depends on the pace at which AI substitutes for cognitive labor in practice, not just in benchmark performance — a distinction that remains unresolved in the economics literature.