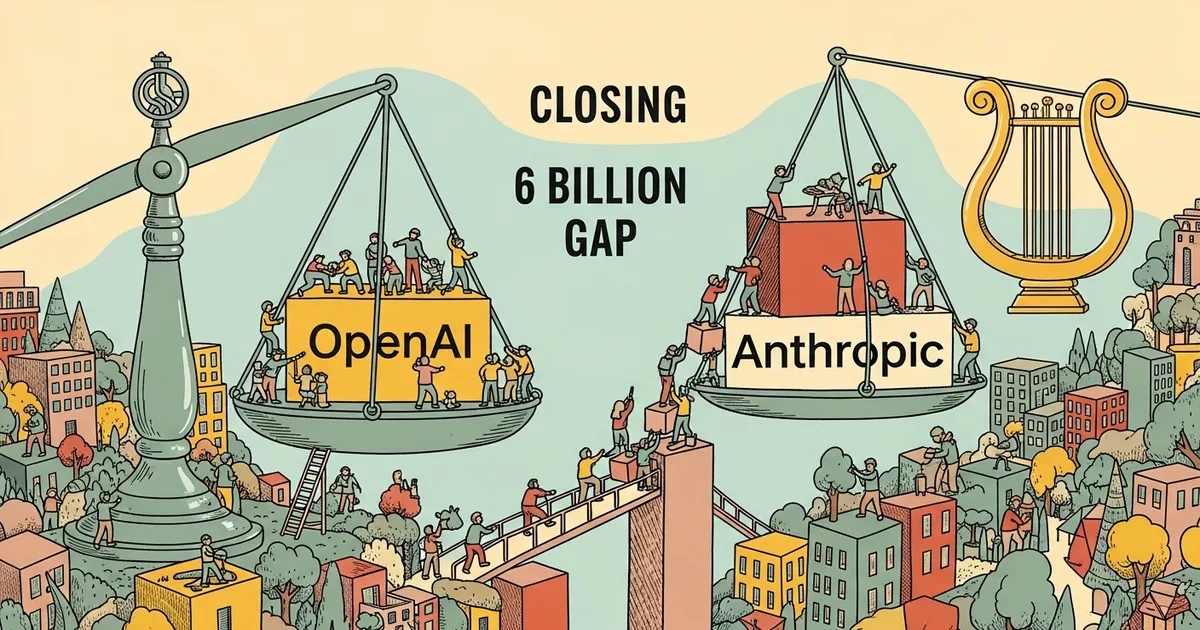

- OpenAI reached $25 billion in annualized revenue by the end of February 2026, growing 17% in just two months from its previous reported level.

- Anthropic surged to nearly $19 billion in annualized revenue, narrowing the gap to $6 billion, with Claude Code alone generating $2.5 billion annually.

- Anthropic’s revenue is growing at roughly 10x per year versus OpenAI’s 3.4x, and its enterprise API market share rose from 12% to 32% while OpenAI’s dropped from 50% to 25%.

What Happened

OpenAI hit $25 billion in annualized revenue at the end of February 2026, according to a report by The Information. That figure represents 17% growth in just two months from its previous reported level, continuing a trajectory that has made OpenAI the fastest-growing technology company by revenue in recent history.

But the more notable number belongs to Anthropic. The Claude maker surged to nearly $19 billion in annualized revenue during the same period, compressing the gap between the two companies to just $6 billion. A year ago, OpenAI’s lead was substantially wider, and Anthropic was still viewed primarily as a research lab with a promising but smaller commercial operation.

The convergence is not incremental. It reflects fundamentally different growth rates that, if sustained, would flip the revenue ranking within months.

Why It Matters

The revenue convergence signals a structural shift in the AI market rather than a temporary fluctuation. Anthropic is growing at approximately 10x per year compared to OpenAI’s 3.4x. At those trajectories, Epoch AI projects Anthropic could surpass OpenAI in annualized revenue by mid-2026, a scenario that seemed implausible even six months ago.

The enterprise API market tells the same story from a different angle. OpenAI’s share of enterprise API revenue dropped from 50% to 25%, while Anthropic’s rose from 12% to 32%. This is not developer experimentation — it reflects production deployments at scale, where companies are choosing Claude over GPT for their core AI infrastructure. For companies building AI into their products, the choice of foundation model provider is no longer a default decision.

Technical Details

Claude Code, Anthropic’s AI coding assistant, is generating $2.5 billion in annualized revenue on its own. That single product line accounts for roughly 13% of Anthropic’s total revenue and has become one of the most significant drivers of the company’s commercial growth. The product’s success demonstrates demand for AI tools that integrate directly into developer workflows rather than operating as standalone chatbots.

Both companies remain unprofitable despite their revenue figures. OpenAI does not expect to break even until 2030, reflecting both its massive infrastructure costs and its heavy investment in frontier model research. Anthropic is targeting breakeven by 2028, two years earlier on the path to sustainable operations. The difference in profitability timelines reflects their revenue mix: Anthropic’s API-heavy business carries different margin profiles than OpenAI’s consumer subscription model, which requires significant spending on user acquisition and retention.

Infrastructure costs remain the dominant expense for both companies, with GPU compute for training and inference consuming the majority of revenue. Neither company has disclosed detailed cost breakdowns, making it difficult to assess which is closer to unit economics sustainability.

Who’s Affected

Enterprise customers choosing between foundation model providers now face a genuinely competitive landscape. Anthropic’s gains in API market share suggest that large-scale production deployments are shifting, not just pilot projects and developer experimentation. The shift has implications for pricing, support commitments, and long-term platform stability.

Investors in both companies are watching the revenue crossover projections closely, particularly as OpenAI prepares for a potential IPO. The valuation dynamics change significantly if Anthropic overtakes OpenAI on revenue before that IPO closes. Developers building on either platform should note the market share shifts, as a provider’s commercial trajectory affects long-term API pricing stability, feature investment, and the likelihood of breaking changes.

What’s Next

The next quarter will determine whether Anthropic’s growth rate holds or decelerates as it scales into larger revenue numbers. Sustaining 10x annual growth from a $19 billion base requires a fundamentally different scale of customer acquisition and infrastructure expansion than growing from $2 billion did. OpenAI’s IPO preparations add pressure to demonstrate accelerating growth and a credible path to profitability. The $6 billion gap is closing, but neither company is profitable yet, and the economics of frontier AI development remain unproven at this scale.